Everyone is turning towards the stock markets these days and trading is one skill that youngsters and even middle-aged people want to learn today in order to create an additional source of income.

There are various types of trading such as:

- Intraday trading: Buying and selling shares on the same day.

- Delivery-based trading: Holding shares for longer than a day before selling them.

- F&O trading: Trading financial derivatives and speculating on the price movements of an underlying asset without actually owning it.

How is income from trading categorised?

When you trade in segments like intraday and F&O, the profits are taxed as income from business.

Why? Because any activity done with the intention of earning profits is considered a business.

Hence, your trading income will be reported as “income from business or profession” head.

Now, depending on the nature of your trading activity, it is categorised into two types:

- Speculative business income

- Non-speculative business income

Intraday transactions are considered speculative since you trade without taking delivery of the contract, that is, the stocks are not delivered to your demat account. This is obviously quite risky and hence, profit from these trades is termed as speculative business income.

Income from other trading activities like delivery-based equity trades, F&O, commodity and currency trades falls under non-speculative business income.

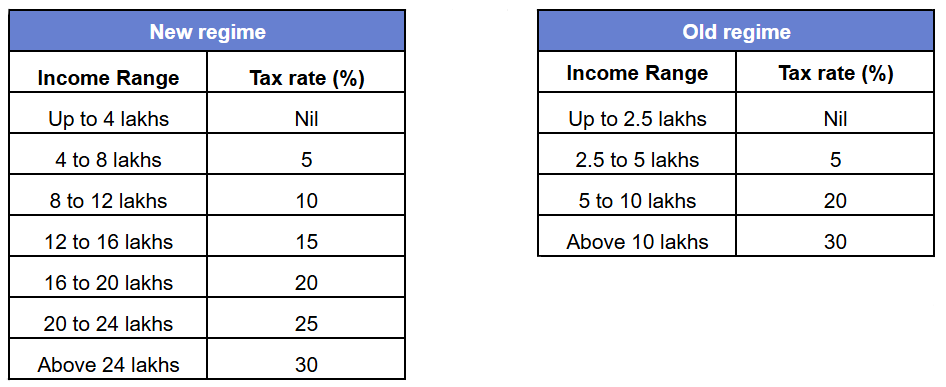

How is income from trading taxed?

Income from trading, both speculative and non-speculative, is added to your overall income, which includes sources like salary, bank interest, rental income and other business income.

The taxes are then determined based on your applicable income tax slab. Here are the tax rates under both the new and the old regime for your reference.

Now, just like a regular business, you can claim expenses you incur related to your trading business like your electricity bills, office rent, internet bills, etc.

Here’s a list of expenses that a trader can claim.

You’ll be liable to pay taxes on the profits that you earn from trading, but what if you incur losses?

Setting off & carrying forward trading losses

Businesses are volatile and you can face losses. If you do so, you can do two things:

- Set off these losses with gains from other income sources in the same year.

- You can carry forward trading losses for a certain number of years and set them off against potential profits in the future.

But there are a few key considerations:

- Non-speculative losses, such as those from F&O trades, can be set off against any other income head except salary income in the same financial year. This includes capital gains, interest income, rental income, etc.

- You can carry forward non-speculative losses for 8 years but once carried forward, the losses can be set off only against other business income (including speculative and non-speculative).

- Speculative losses, on the other hand, like those from intraday trading, can only be set off against other speculative profits.

- Also, speculative losses can be carried forward for 4 years and set off only against future speculative profits.

Tax Audit Applicability

Every business is required to maintain books of accounts and financial statements, and so are traders. And tax “audit” basically means getting these books of accounts inspected by a practising CA.

The tax audit applicability depends on the trading turnover. Along with the turnover limits, there are certain other conditions attached to it as well to determine Tax audit applicability. Here’s a detailed read on tax audit applicability.

According to Section 44AB of the Income Tax Act, a business is required to have a tax audit carried out if the sales, turnover or gross receipts of the business exceed ₹1 crore in a financial year.

However, this threshold limit increases from ₹1 crore to ₹10 crore in case cash receipts and cash payments made during the year do not exceed 5% of the total receipts or payments.

Since intraday and F&O transactions are 100% digital in nature, the turnover limit for a tax audit is ₹10 crores for traders.

How is trading turnover calculated?

In the case of both intraday and F&O trading, the turnover is calculated as the absolute sum of all profit and loss from the transactions. This means that you add the value of all profits and losses without taking the -ve sign into consideration. Let’s take a simple example. You made three trades, had profit in the first two and a loss in the third.

So, your turnover becomes ₹120. Simple.

Which ITR form needs to be filed?

It’s mandatory to file your ITR if you have any trading transactions. Moreover, if you have losses and want to carry them forward, you will have to file the ITR before the due date which is 31st August of the respective assessment year for ITR-3 or ITR-4.

In case you fall under the Audit umbrella, you will have to get the audit done and submit the tax audit report on or before 30th September of the relevant assessment year. And the last date to submit the ITR in this case will be 31st October.

ITR 3 and ITR 4 are applicable for traders since income from trading is categorized as business income.

For the majority of the intraday and F&O traders, ITR 3 is applicable unless they have opted for the presumptive taxation scheme.

From AY 2026–27 onwards, ITR-3 introduces two new fields specifically for F&O reporting:

- 12c: Turnover from Futures & Options Trading

- 12d: Income from F&O Trading (transferred to P&L)

These sit alongside the existing fields 12a and 12b for intraday trading. These new fields give you clearer places to report turnover and income separately, reducing the chance of filing errors or mismatches with broker data.

These sit alongside the existing 12a and 12b fields for intraday trading. With separate fields for F&O turnover and income, it will become easier to report your F&O activity more accurately and keep it aligned with your broker statements so there are fewer chances of mismatches while filing.

Switching between old and new regime

As the new regime has been made the default regime from 1st April 2023 onwards, if you decide you want to opt for the old regime, you will have to file form 10IEA to switch from the new regime to the old regime.

Here’s a video guide on taxation for traders.

If you have any further queries, ask us below!